Straddles vs. Strangles: The Earnings Vol Play

Straddles vs. Strangles: The Earnings Vol Play

Here’s a trade that doesn’t care which way the stock moves. The company could beat earnings by a mile or miss badly — and you’d profit from either outcome. You only need one thing: the stock has to move. Decisively.

That’s the core idea behind straddles and strangles — directional-neutral volatility strategies built for binary events like earnings announcements, drug approvals, and major macro releases. They’re the first true intermediate strategy on this blog, and they require thinking about options not in terms of direction, but in terms of magnitude.

The Core Concept: Betting on Movement, Not Direction

Most investors think in directional terms: “I think the stock goes up” or “I think it goes down.” But there’s a third view: “I don’t know which way it goes, but it’s going to move a lot.”

That view is tradeable. By buying both a call and a put simultaneously, you profit from a large move in either direction. You pay premium for both options, so you need the move to exceed your combined premium cost to profit. But if the stock makes a big enough swing, the winning side gains far more than the losing side loses.

This is a long volatility strategy — you’re buying the right to be surprised.

The Long Straddle

A straddle buys one call and one put at the same strike price — typically at-the-money (ATM) — on the same underlying stock with the same expiration.

Example setup with stock at $150:

- Buy 1x $150 call, expiring in 14 days: premium $7.00

- Buy 1x $150 put, expiring in 14 days: premium $7.00

- Total cost: $14.00/share = $1,400 per straddle

- Break-even at expiration: $136 (below) or $164 (above)

The straddle costs more but profits from smaller moves because both options are at-the-money. The maximum loss of $1,400 occurs only if the stock closes exactly at $150 at expiration — the ideal scenario for whoever sold you those options.

The Long Strangle

A strangle buys an OTM call at a higher strike and an OTM put at a lower strike. It costs less than a straddle because neither option has intrinsic value.

Example setup with stock at $150:

- Buy 1x $160 call, expiring in 14 days: premium $4.00

- Buy 1x $140 put, expiring in 14 days: premium $4.00

- Total cost: $8.00/share = $800 per strangle

- Break-even at expiration: $132 (below) or $168 (above)

The strangle is cheaper but requires a larger move to profit. The stock must exceed the wider break-evens before you see gains.

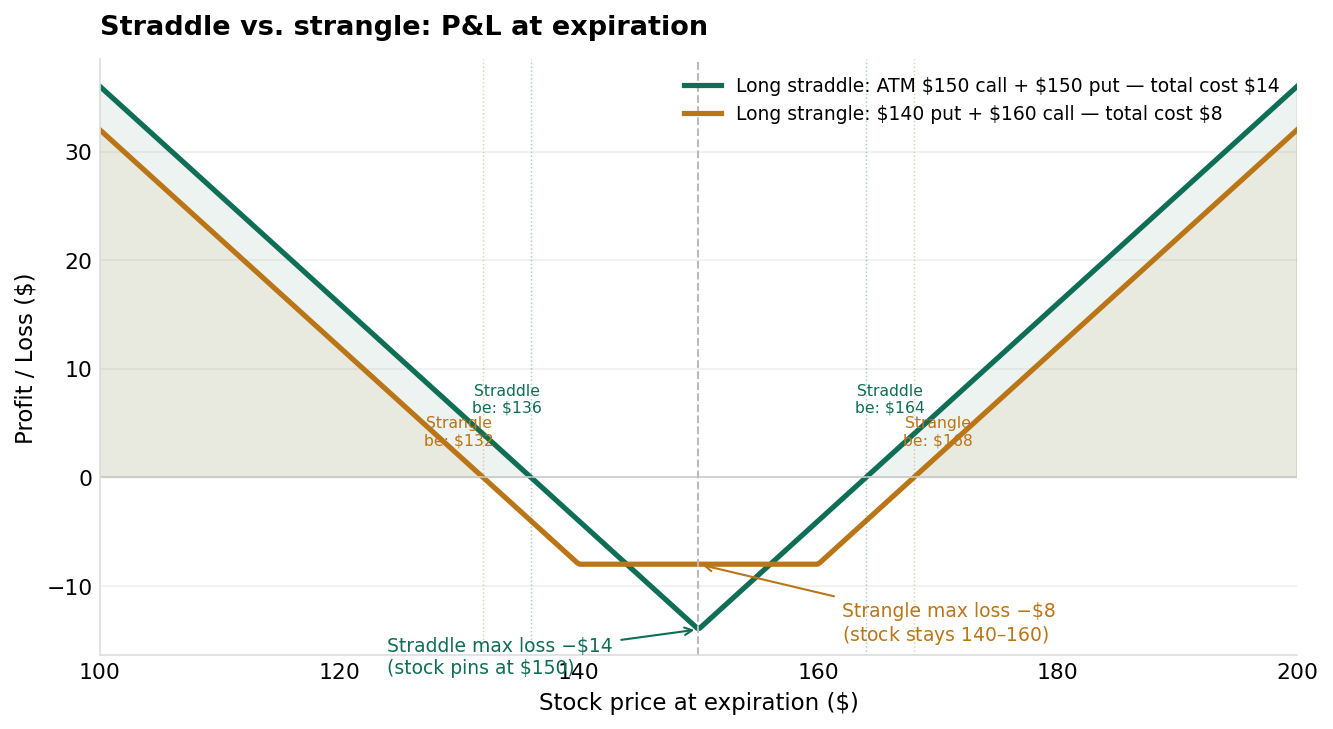

Side by Side at Expiration

The straddle (teal) starts profiting from smaller moves but costs $14 and has a tighter break-even range. The strangle (amber) costs only $8 but needs a bigger move — $132 or below, $168 or above — to turn a profit.

The straddle (teal) starts profiting from smaller moves but costs $14 and has a tighter break-even range. The strangle (amber) costs only $8 but needs a bigger move — $132 or below, $168 or above — to turn a profit.

The chart tells the full story at a glance:

- Both strategies lose money if the stock barely moves

- The straddle’s V-shape is centered and narrower — it starts winning sooner but costs more

- The strangle’s V-shape is wider — it needs a bigger swing but was cheaper to enter

- Both strategies have limited loss (the premium paid) and theoretically unlimited upside on the call side

The Trade-Offs: Straddle or Strangle?

| Factor | Straddle | Strangle |

|---|---|---|

| Upfront cost | Higher ($14) | Lower ($8) |

| Break-even distance | Smaller ($14 from center) | Larger ($18 each side) |

| Profits from smaller moves | Yes | No — needs bigger swing |

| Maximum loss | Higher ($1,400) | Lower ($800) |

| Best when you expect | A moderate-to-large move | A very large move |

| Sensitivity to IV crush | Very high (ATM) | Moderate (OTM) |

As a rule: use straddles when you expect a decisive but not extreme move; use strangles when you expect a truly large, gap-type move.

The Elephant in the Room: IV Crush

Here’s the problem most beginners don’t see coming. Before earnings, implied volatility (IV) spikes as traders buy options to position for the event. Option prices are richly inflated. On the morning after the announcement, IV collapses — even if the stock made a meaningful move.

This IV crush can partially or fully offset your gains from the directional move. If the $150 straddle cost $14 before earnings with IV at 80%, and IV collapses to 35% the next morning, the options are repriced at a fraction of their prior value — even before the stock’s move is fully accounted for.

The math has to work on both fronts:

- The stock move must exceed the break-even and

- The move must be large enough to overcome the IV crush

This is why straddle buyers often get burned even when they’re right about direction. The market was already pricing in a big move — the implied move was priced in. You need to be more right than the options market.

Calculating the implied move: Before earnings, take the ATM straddle price and divide by the stock price.

Straddle price $14 ÷ Stock price $150 = ~9.3% implied move

The market is saying it expects roughly a 9.3% swing. If you think the actual move will be larger, buy the straddle. If you think it’ll be smaller, sell the strangle (see below).

The Short Side: Selling the Strangle Before Earnings

If IV reliably spikes before earnings and reliably collapses after — which it does, as we covered in Vega and Earnings — then selling the strangle before the announcement is the trade that captures the IV premium.

Setup: Sell both OTM options before earnings, aiming to buy them back cheaply after the collapse:

- Sell 1x $160 call for $4.00

- Sell 1x $140 put for $4.00

- Total premium collected: $800

- Profit if stock stays between $132 and $168 at expiration

The risk is significant: if the stock gaps beyond the break-evens, you face mounting losses. This is why professional earnings volatility sellers use defined-risk variations — iron condors or short strangles with protective wings — rather than naked strangles.

Short strangles around earnings are not for beginners. They require precise sizing, a deep understanding of the stock’s historical earnings move, and a risk management plan before entry.

When to Use Each Strategy

Buy a straddle when:

- You have high conviction the stock will make a large move (not just “it might move”)

- The implied move seems underpriced relative to the stock’s historical earnings moves

- You’re willing to accept IV crush in exchange for a potential large directional payoff

Buy a strangle when:

- You want the same bet at lower cost and can accept requiring a larger move to profit

- The stock has a history of gap moves significantly larger than the options market implies

- You want lower maximum loss exposure

Sell a strangle when:

- You have a clear view that the implied move is overpriced

- You’re trading with defined risk (iron condor) to cap your worst-case scenario

- You understand and accept that a tail-risk event can cause severe losses

Position Sizing for Volatility Plays

Volatility trades around binary events are inherently binary — the move either happens or it doesn’t. Treat them as speculative positions:

- Size no more than 2–5% of your portfolio per trade

- Never risk more than you’re prepared to lose entirely

- Close losing positions when they hit 2× the premium paid — don’t hold a straddle that’s lost most of its value hoping for a late reversal

- Take profits quickly on winners (50–75% gain) — IV crush and theta work against you constantly

Key Takeaways

- A long straddle buys ATM call + ATM put on the same stock — profits from any large move in either direction; costs more but has tighter break-evens

- A long strangle buys OTM call + OTM put — costs less but needs a larger stock move to profit; wider break-evens

- Both strategies have limited, defined risk (the premium paid) and profit from large moves in either direction

- IV crush is the biggest enemy of long vol buyers: the implied move is already priced in, and IV collapses after the announcement regardless of direction

- Use the implied move formula (straddle price ÷ stock price) to benchmark whether the expected move is fairly priced before taking a position

- Selling strangles before earnings is the inverse trade — it captures the IV premium but carries large tail-risk and requires defined-risk structures for most traders

What’s Next

You’ve now completed the first ten articles of The Greeks Lab — from “what is an option” all the way to earnings volatility strategy. Next quarter, we expand into spreads — defined-risk structures that let you sell premium with a built-in safety net — starting with the Bull Put Spread.

Welcome to intermediate territory.

For trading straddles and strangles around earnings, Tastytrade is where most volatility traders operate — their platform shows the implied move, IV rank, and the full Greeks side-by-side so you can quickly evaluate whether the straddle is overpriced or fairly valued before you trade.

Disclosure: this is a referral link. If you sign up via this link, the site may earn a commission at no cost to you.

Disclaimer: This content is for educational and informational purposes only and does not constitute financial, investment, or trading advice. Options trading involves significant risk and is not suitable for all investors. You may lose the entire amount invested. Options strategies involving the sale of uncovered options carry theoretically unlimited risk and are suitable only for sophisticated investors with high risk tolerance. Always conduct your own research and consult a licensed financial advisor before making investment decisions.