Theta Decay: The Options Seller's Best Friend

Theta Decay: The Options Seller’s Best Friend

Every day that passes is money in the pocket of an options seller. This is theta — the Greek that makes time your ally, and the reason why selling options is often described as having the equivalent of a casino’s edge over the long run.

If you’ve ever bought an option and watched it lose value even though the stock didn’t move, you’ve experienced theta from the wrong side. This article puts you on the right side of it.

What Is Theta?

Theta (Θ) measures how much value an option loses for each day that passes, all else being equal.

An option with a theta of −0.05 loses approximately $0.05 per share ($5 per contract) in value each day, simply from the passage of time. The stock doesn’t have to move. Nothing else has to happen. The calendar advances, and value drains out of the option.

For the buyer, theta is a constant headwind. Every morning, their option is worth slightly less than the night before.

For the seller, theta is a tailwind. Every morning, the option they sold is worth slightly less — which means it costs less to buy back, generating a profit.

This is why the options income community sometimes calls theta “the invisible paycheck.”

Why Time Value Exists

An option has value for a simple reason: as long as time remains, there is some probability that the stock could move to make the option profitable. The more time remaining, the more possibilities. The less time remaining, the fewer possibilities.

This probabilistic component — the portion of an option’s price that is not intrinsic value — is called time value (also called extrinsic value). It is the portion that theta erodes.

An out-of-the-money option is composed entirely of time value. When it expires worthless, the seller keeps every penny of the premium — that was all time value, and all of it decayed away.

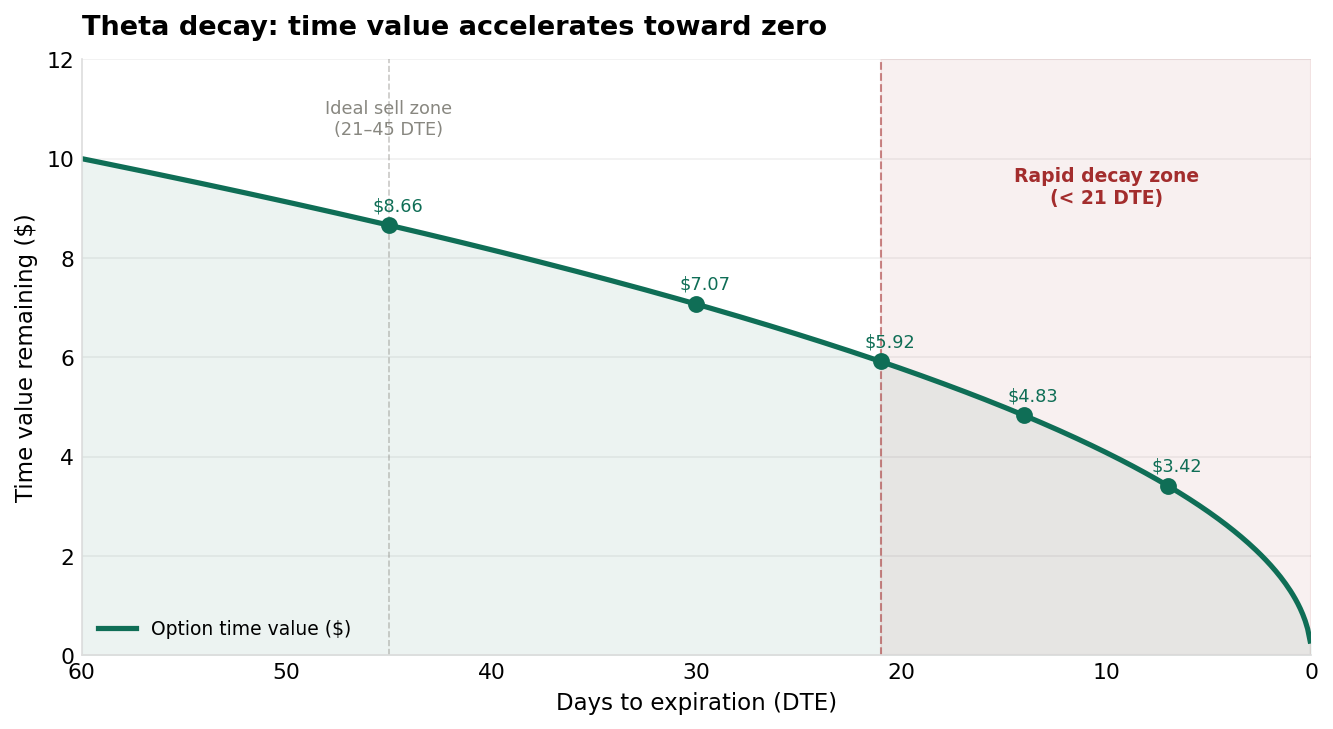

The Decay Curve: Why It Accelerates Near Expiration

Here’s where the insight gets powerful: theta decay is not linear. It accelerates as expiration approaches.

An option’s time value decays slowly when there are 60 days left, and rapidly in the final 21 days. The “rapid decay zone” is highlighted in red.

An option’s time value decays slowly when there are 60 days left, and rapidly in the final 21 days. The “rapid decay zone” is highlighted in red.

Notice the shape of the curve:

- With 60 days to go, the option retains most of its time value — decay is slow

- At 30 days, decay is moderate and picking up pace

- Inside 21 days, decay accelerates dramatically — the curve steepens sharply

- In the final week, the option can lose half its remaining time value in a matter of days

This curve shape is why experienced sellers use the phrase “inside 21 DTE, things get spicy.” The acceleration of theta cuts both ways: sellers are collecting faster, but the position becomes more sensitive to stock moves (remember gamma from the delta article).

The Sweet Spot: 21–45 Days to Expiration

The decay curve leads to a widely-accepted rule among options income traders: sell options with 30–45 days to expiration (DTE) and close them when they’ve decayed to 50% of their original value (typically around 21 DTE).

Here’s the logic:

Why not sell further out (60+ DTE)? The option has more premium, but you’re collecting it slowly. Your capital is tied up for a long period in a trade that isn’t decaying fast enough to justify the wait. Return on capital is lower.

Why not sell very close (7–14 DTE)? Theta decay is fastest here, but gamma risk spikes dramatically. A small, unexpected stock move can wipe out weeks of premium collection in a single session.

The 30–45 DTE zone captures the beginning of the steeper decay curve while maintaining reasonable gamma risk. You collect meaningful premium over 2–3 weeks, close the position at 50% profit (21 DTE or so), and redeploy into a fresh 30–45 DTE trade. Repeat.

The 50% Profit Rule: Close Early, Trade Often

Many professional sellers use the 50% profit target as their standard exit:

- Sell a put for $4.00 → target to buy it back for $2.00

- That’s 50% of max profit in roughly half the time remaining

- Once closed, immediately open a new position in the next expiration cycle

Why not hold to expiration and collect the full premium? Because the remaining 50% of profit typically requires holding through the riskiest portion of the option’s life — the final 21 days of high gamma. The risk-adjusted return is better by closing early and opening a fresh trade with a full 30–45 DTE runway.

Over many trades, the math favors the disciplined seller who makes ten 50%-profit trades over the gambler holding each position to the wire.

What Theta Looks Like on Real Positions

Let’s put numbers to a real trade to see theta in action.

You sell an AAPL $165 put with 35 DTE for $4.00, receiving $400 per contract. The option has a theta of −$0.09 per day.

| Day | Days Remaining | Approx. Time Value | Daily Theta Collected |

|---|---|---|---|

| Day 0 (entry) | 35 DTE | $4.00 | — |

| Day 7 | 28 DTE | $3.35 | ~$0.09/day |

| Day 14 | 21 DTE | $2.60 | ~$0.11/day (accelerating) |

| Day 21 | 14 DTE | $1.80 | ~$0.14/day |

| Day 28 | 7 DTE | $0.90 | ~$0.19/day |

| Day 35 | 0 DTE | $0.00 | Full decay |

Notice how the daily collection accelerates from $0.09 at the start to $0.19 in the final week — exactly what the curve showed. Following the 50% rule, you’d close around Day 14 (buying back for ~$2.00), capturing $200 profit per contract in about two weeks, then start fresh.

Theta and Volatility: The Important Relationship

There’s a catch: options with higher implied volatility have higher theta. More time value = more to decay. This is actually good news for sellers — periods of elevated volatility mean fatter premiums with faster decay.

We’ll explore this deeply in the Vega and Earnings article, but for now, understand that theta and vega are opposing forces: volatility pumps up option prices; time decay drains them. As a seller, you’re taking the “time beats volatility” side of that bet.

Key Takeaways

- Theta measures daily time value decay — sellers collect it, buyers pay it

- Time value decay is not linear — it accelerates as expiration approaches, especially inside 21 DTE

- The 30–45 DTE window is the professional sweet spot: meaningful premium, manageable gamma risk

- The 50% profit rule — close at half the premium collected, redeploy immediately — maximizes risk-adjusted return over many trades

- Options with higher implied volatility have higher theta — fatter premiums for sellers in volatile markets

What’s Next

You now understand why time works for sellers. Next, let’s explore the most dramatic example of time value and volatility interacting: earnings season. Vega and Earnings: Playing Volatility the Right Way explains what IV crush is and how to trade around it.

If you want to put theta decay to work in real trades, Tastytrade is the platform most premium sellers use — it shows theta directly on the options chain, makes it easy to filter for the 30–45 DTE window, and lets you set profit targets to close at 50% with a simple order.

Disclosure: this is a referral link. If you sign up via this link, the site may earn a commission at no cost to you.

Disclaimer: This content is for educational and informational purposes only and does not constitute financial, investment, or trading advice. Options trading involves significant risk and is not suitable for all investors. You may lose the entire amount invested. Always conduct your own research and consult a licensed financial advisor before making investment decisions.