Cash-Secured Puts: Getting Paid to Buy Stocks Cheaper

Cash-Secured Puts: Getting Paid to Buy Stocks Cheaper

Here’s a scenario every investor has faced: you see a stock you love — solid company, great fundamentals — but it’s trading 10% higher than the price you’d want to pay. So you wait. And while you wait, you earn nothing.

Cash-secured puts change that entirely. Instead of sitting on cash and hoping for a dip, you collect real premium income while you wait. And if the stock dips to your target price, you buy it at the discount you wanted — minus the premium you already collected.

It’s one of the most elegant strategies in options trading, and it’s often the first trade new options traders should learn.

How a Cash-Secured Put Works

When you sell a cash-secured put, you’re selling someone else the right to sell their shares to you at a specific price before expiration. In exchange, they pay you a premium.

You hold enough cash in your account to buy 100 shares at the strike price if the option is exercised (hence “cash-secured”). This is what makes the risk profile equivalent to simply placing a limit order to buy stock — except that limit order pays you while you wait.

The two outcomes:

-

Stock stays above your strike: The put expires worthless. You keep the full premium. The stock didn’t fall to your target price, so you didn’t buy it — but you got paid for being willing to.

-

Stock falls to or below your strike: The put is exercised. You’re “assigned” — you buy 100 shares at the strike price. But your effective cost is the strike price minus the premium received. You bought the stock cheaper than the strike, and cheaper than it was trading when you sold the put.

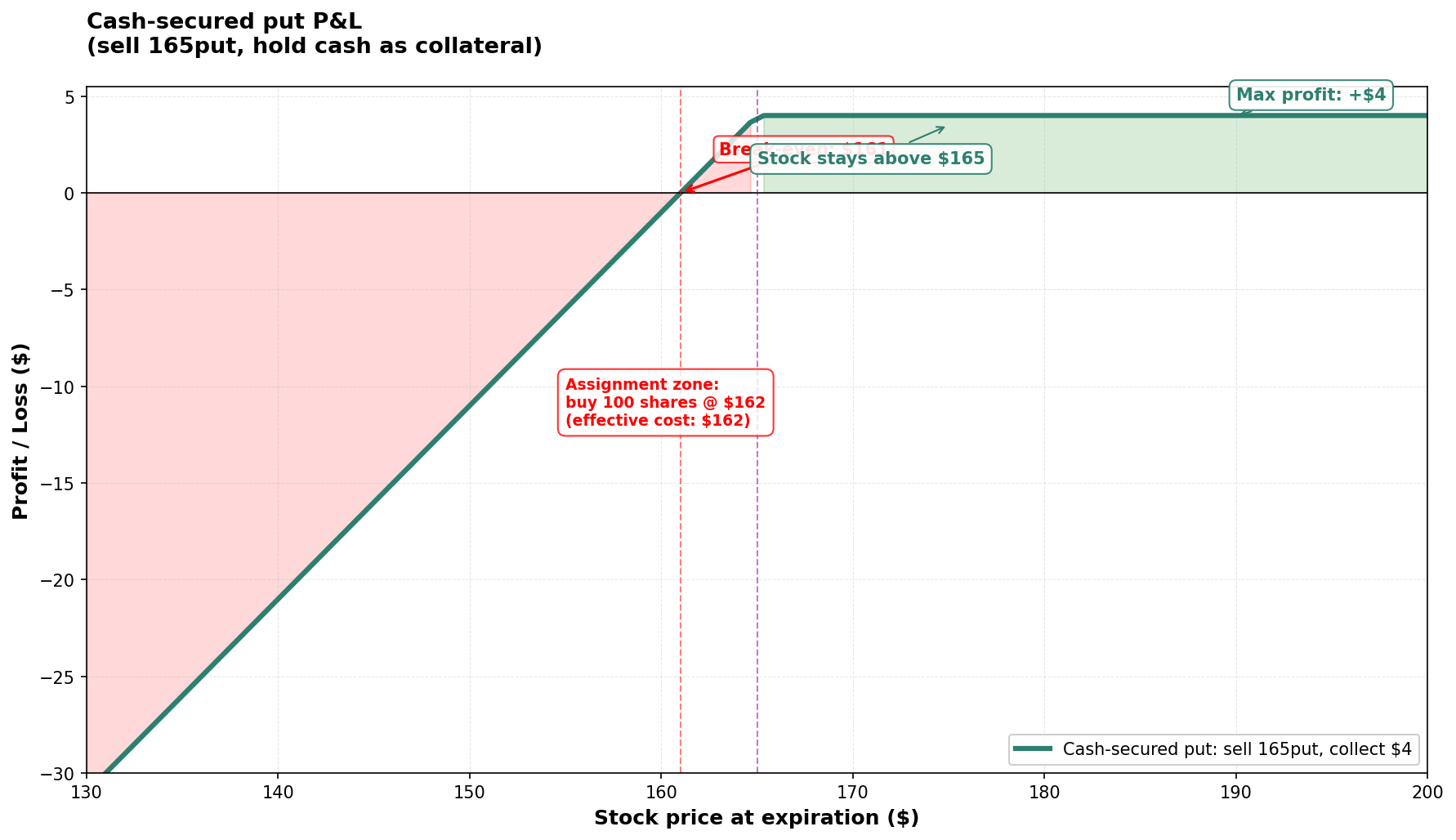

A Real Trade: AAPL at $170

Suppose AAPL is trading at $170 and you’d like to own it at $165 or below. You think it’s a great company and wouldn’t mind buying at that level.

Trade setup:

- Sell 1x AAPL $165 Put, expiring in 35 days

- Premium received: $4.00/share = $400 credited to your account immediately

- Cash held as collateral: $16,500 (to buy 100 shares at $165 if assigned)

Maximum profit is the $4 premium — earned if AAPL stays above $165. If assigned, effective purchase price is $161 (strike minus premium). Break-even is $161.

Maximum profit is the $4 premium — earned if AAPL stays above $165. If assigned, effective purchase price is $161 (strike minus premium). Break-even is $161.

Outcomes at expiration:

| Scenario | Stock at Expiry | Action Taken | P&L |

|---|---|---|---|

| AAPL stays above $165 | $170–$200+ | Put expires worthless, keep $400 | +$400 |

| AAPL slightly below strike | $163 | Assigned at $165, effective cost $161, current value $163 | +$200 (paper gain) |

| AAPL at break-even | $161 | Assigned at $165, effective cost $161, same as market | $0 |

| AAPL falls moderately | $150 | Assigned at $165, effective cost $161, paper loss | −$1,100 |

| AAPL falls hard | $130 | Assigned at $165, effective cost $161, paper loss | −$3,100 |

The maximum gain is $400 — the premium collected. The maximum loss is substantial ($16,100, if AAPL went to zero), but it’s identical to the loss you’d suffer if you’d simply bought the stock outright at $165. The premium merely reduces your effective cost.

Break-Even and the Effective Purchase Price

Two numbers to always calculate before entering a CSP:

Break-even = Strike − Premium received

In our example: $165 − $4 = $161. The stock needs to fall below $161 before you’re truly underwater relative to a cash investor.

Effective purchase price = Strike − Premium (if assigned)

You acquire the shares at a cost basis of $161 — lower than both the strike and the current stock price. This is the “getting paid to buy at a discount” aspect of the strategy.

Choosing Your Strike

Strike selection for cash-secured puts follows similar principles to covered calls:

Target the 0.25–0.35 delta range, 30–45 DTE. For AAPL at $170, the 0.30-delta put typically sits around $160–$165 depending on current implied volatility.

The lower the strike, the less premium you collect — but the lower your purchase price if assigned and the lower your probability of assignment.

Ask yourself: “Am I happy owning this stock at this price, long-term?” If the answer is yes, the strike is appropriate. If you’d feel “stuck” buying at that price in a downturn, choose a lower strike or a different underlying.

Never sell a CSP on a stock you don’t want to own. This is the cardinal rule. Unlike other strategies, a CSP can result in actual stock ownership. If you’re assigned shares of a company you don’t believe in, you’re in trouble.

What Happens When You’re Assigned?

Assignment means the put was exercised — the stock fell below your strike, and you bought 100 shares at the strike price. Here’s what to do next:

Step 1: Check your thesis. Did the stock fall because of broader market weakness (temporary) or company-specific bad news (potentially structural)? This changes your next move entirely.

Step 2: Check your effective cost basis. Your cost basis is the strike minus the premium received ($161 in our example). If the stock is at $158, you’re showing a $300 paper loss — but you entered with a bullish thesis, so you hold.

Step 3: Sell a covered call. Now that you own 100 shares, sell a covered call against them to continue collecting premium and reduce your cost basis further. This is the beginning of the Wheel Strategy.

CSP vs. Limit Order: Why the Option Is Better

Some investors say: “Why not just place a limit buy order at $165?” It’s a fair question.

The difference: a limit order earns you nothing while you wait. A cash-secured put earns you $400 immediately. If the stock never reaches $165, the limit order never fills and you earned nothing. The CSP also doesn’t fill — but you collected $400.

The only downside: the CSP requires you to actively manage positions, roll them when needed, and accept potential assignment. A limit order is more set-it-and-forget-it. But in terms of returns on committed capital, the CSP wins.

Cash Requirement: The Capital Commitment

Unlike covered calls (which require owning shares), a CSP requires holding cash — or, in a margin account, owning sufficient collateral. Most brokers require you to hold the full purchase price as a cash reserve.

For our AAPL trade: $165 × 100 = $16,500 in reserved capital. Your yield on this capital: $400 / $16,500 = 2.4% for 35 days, or roughly 25% annualized if repeated consistently.

This is why position sizing matters: avoid committing too much capital to any single CSP, especially on volatile underlying stocks.

Key Takeaways

- A cash-secured put is selling the right to “put” shares to you at a chosen strike, in exchange for immediate premium

- Two outcomes: stock stays above strike (keep premium, no shares) or stock falls below strike (buy shares at a discount)

- Effective purchase price = Strike − Premium; this is always lower than the strike you committed to

- Target 0.25–0.35 delta, 30–45 DTE for a balance of premium and probability

- Only sell CSPs on stocks you genuinely want to own at the chosen strike — assignment is a real possibility

- A CSP generates income that a plain limit order cannot; on capital reserved for potential stock purchases, it’s almost always superior

What’s Next

You’ve now learned both sides of options income: covered calls (own the stock, sell the call) and cash-secured puts (want the stock, sell the put). The Wheel Strategy: A Full Income Cycle Explained shows you how to chain them together into a seamless income machine.

To sell cash-secured puts with confidence, Tastytrade is the go-to platform for premium sellers — low commissions on options, real-time buying power updates as you select strikes, and a margin display that shows exactly how much capital your CSP will reserve.

Disclosure: this is a referral link. If you sign up via this link, the site may earn a commission at no cost to you.

Disclaimer: This content is for educational and informational purposes only and does not constitute financial, investment, or trading advice. Options trading involves significant risk and is not suitable for all investors. You may lose the entire amount invested. Always conduct your own research and consult a licensed financial advisor before making investment decisions.