The Wheel Strategy: A Full Income Cycle Explained

The Wheel Strategy: A Full Income Cycle Explained

The wheel is not a single trade. It’s a system. It chains two strategies you already know — cash-secured puts and covered calls — into a repeating income loop that generates premium at every step, whether the stock goes up, stays flat, or dips to your buy zone.

Many traders describe the wheel as the closest thing options has to a “passive income machine” — and while no strategy is truly passive, the wheel is methodical, predictable, and executable by anyone who understands the two building blocks.

The Core Idea

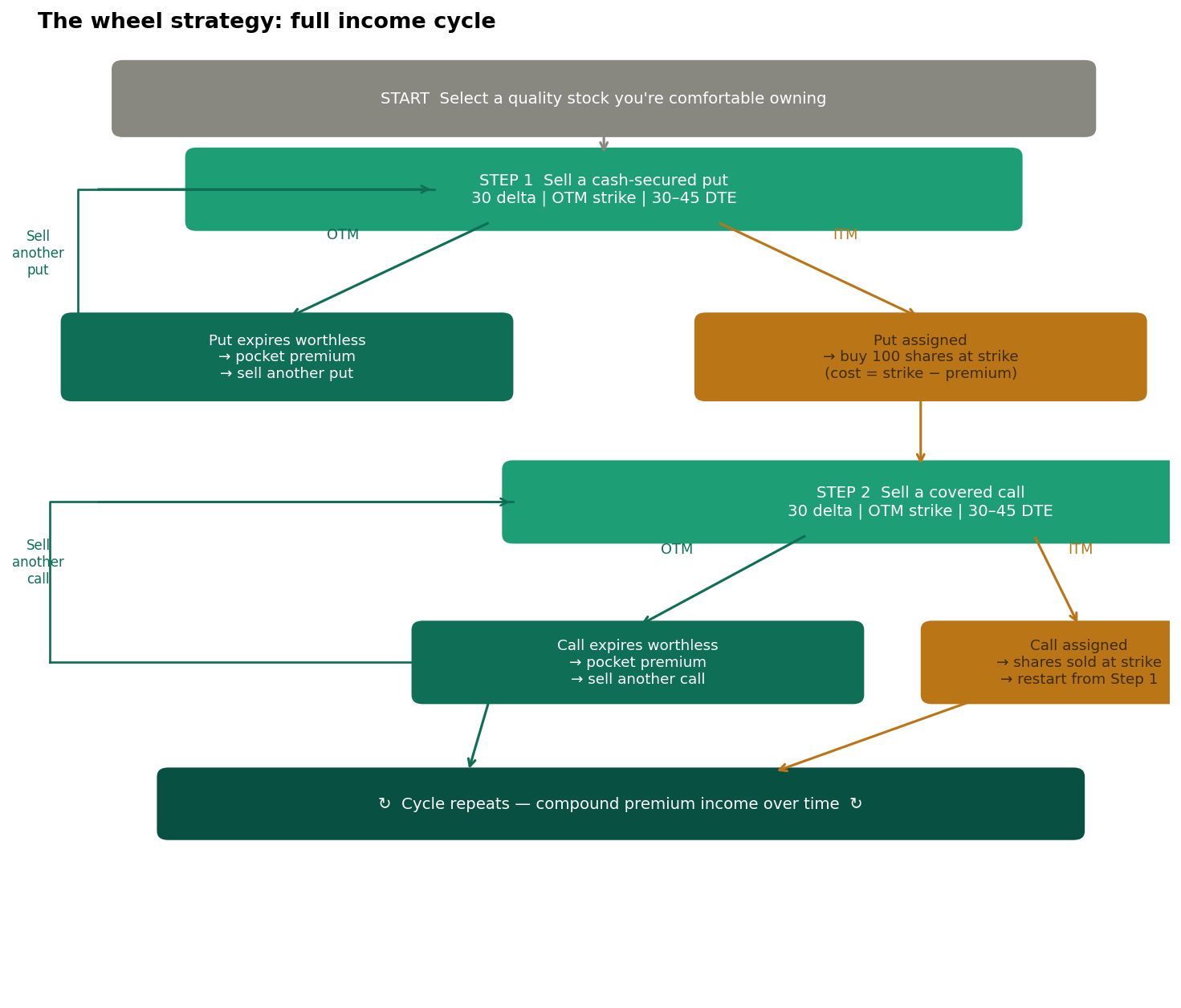

The wheel runs in two modes, and you’re always in one of them:

- No shares: Sell cash-secured puts. Collect premium. Wait to be assigned.

- Own shares: Sell covered calls. Collect premium. Wait to be called away.

Repeat indefinitely.

If the stock behaves — stays range-bound, drifts sideways, or trends mildly — you collect premium in both phases without ever being forced to take a big loss. The income compounds over time.

The Full Cycle, Step by Step

The wheel cycles between selling cash-secured puts (when you hold cash) and selling covered calls (when you hold shares). Each path collects premium; the cycle repeats.

The wheel cycles between selling cash-secured puts (when you hold cash) and selling covered calls (when you hold shares). Each path collects premium; the cycle repeats.

Step 1: Select Your Stock

The wheel starts with stock selection — and this is more important than any options mechanic.

You need a stock that:

- You genuinely want to own at the put strike you plan to sell (critical — assignment is real)

- Has liquid options (tight bid/ask spreads, reasonable volume)

- Is in a sideways to mildly bullish trend — wild momentum stocks can run through your call strikes or crater through your put strikes in a single session

- Is not reporting earnings in the near term (earnings carry IV crush and gap risk that disrupts the cycle)

Popular wheel candidates: dividend-paying blue chips, broad ETFs (SPY, QQQ), sector leaders (AAPL, MSFT, JPM), and high-quality mid-caps with active options markets.

Step 2: Sell a Cash-Secured Put

Entry target: 0.25–0.35 delta, 30–45 DTE, OTM strike

Using AAPL at $170 as our example:

- Sell 1x AAPL $165 Put, 35 DTE

- Premium received: $4.00/share = $400

- Cash held as collateral: $16,500

Two outcomes:

A) Put expires worthless (AAPL stays above $165) AAPL is trading above $165 at expiration. The put expires worthless. You keep the $400 and immediately sell another put for the next cycle. Return to Step 2.

B) Put is assigned (AAPL falls below $165) You buy 100 shares of AAPL at $165. Effective cost basis: $165 − $4 = $161. This is not a loss — this is the stock reaching the price you were willing to buy it at. You now own 100 shares and move to Step 3.

Step 3: Sell a Covered Call

Entry target: 0.20–0.30 delta, 30–45 DTE, OTM strike above your cost basis

You now own 100 shares of AAPL at an effective cost of $161. AAPL is trading at, say, $163 (it dipped slightly when you were assigned).

- Sell 1x AAPL $170 Call, 35 DTE

- Premium received: $4.50/share = $450

- Your new cost basis: $161 − $4.50 = $156.50

Two outcomes:

A) Call expires worthless (AAPL stays below $170) AAPL stays below $170. Your call expires worthless. You keep the $450 and sell another covered call for the next cycle. Return to Step 3.

B) Call is assigned (AAPL rises above $170) Your shares are called away at $170. You sell at $170 with a cost basis of $161. Profit: $900 per contract ($9/share × 100). Plus the $400 and $450 in premiums. Total collected for this full cycle: $1,750 per contract.

After the call assignment, you’re back to holding cash — and you return to Step 2.

A Full Cycle: The Numbers

Here’s a complete wheel cycle on AAPL, end to end:

| Event | Premium / P&L |

|---|---|

| Sell $165 put × 2 cycles (expires worthless twice) | +$800 |

| Assigned at $165, buy 100 shares, cost basis $161 | — |

| Sell $170 covered call × 1 cycle (expires worthless) | +$450 |

| Sell $172 covered call × 1 cycle (assigned, sold at $172) | +$350 |

| Shares sold at $172, cost basis $156.50 | +$1,550 (capital gain) |

| Total premium + gain collected | $3,150 |

| Capital required (peak) | ~$16,500 |

| Total return this cycle | ~19% |

Time elapsed: approximately 3–4 months.

Managing the Wheel: What Can Go Wrong

Problem 1: The Stock Crashes After Assignment

You’re assigned at $165, but the stock falls to $140. Your covered call strike is way above the current price — nobody will pay meaningful premium on a $165 call when the stock is $140.

Options:

- Sell a deep OTM call at $150 or lower to collect something and reduce basis

- Hold patiently and wait for recovery (works best if you chose a fundamentally strong company)

- Accept the loss if your thesis has materially changed

This is why stock selection is so important. If you wheel a stock you’d hold anyway through a 20% drawdown, the loss is manageable. If you wheeled a meme stock or a company with uncertain fundamentals, the wheel becomes a trap.

Problem 2: The Stock Rips Past Your Call Strike

Your covered call was at $170 and the stock ran to $195. Your shares get called away at $170 — you missed $25 in gains.

This is the trade-off of the wheel. The strategy sacrifices explosive upside for consistent income. If you’re bullish enough to want to hold through a major run, the wheel may not be the right vehicle for that position.

Problem 3: Stuck Carrying Shares Through an Earnings Event

If you’re assigned shares right before the company reports earnings, your covered call becomes a volatility event. Price it accordingly, or consider closing the position before the report.

Strike Selection Summary for the Wheel

| Phase | Delta Target | DTE | Goal |

|---|---|---|---|

| CSP | 0.25–0.35 | 30–45 | Collect premium, target buy price slightly below current price |

| Covered Call | 0.20–0.30 | 30–45 | Collect premium, strike above cost basis (aim to profit if called away) |

Critical rule: Your covered call strike should always be at or above your effective cost basis. Never sell a covered call below your cost basis — if assigned, you’d book a guaranteed loss on the shares.

Realistic Return Expectations

The wheel’s annualized return depends heavily on the underlying stock’s volatility and how consistently you execute. Based on historical options pricing:

- Low-volatility stocks (SPY, QQQ): 8–12% annualized premium income

- Mid-volatility stocks (AAPL, MSFT): 12–20% annualized premium income

- High-volatility stocks: 20–35%+ — but with substantially higher risk of large drawdowns

Note: these are premium-only estimates. They don’t account for capital gains when called away, dividends, or potential losses from large stock moves. Past options premiums are not a guarantee of future income.

Key Takeaways

- The wheel chains cash-secured puts (cash phase) and covered calls (stock phase) into a repeating premium income cycle

- Stock selection is the most critical decision — only wheel stocks you genuinely want to own through a downturn

- In the CSP phase: collect premium while waiting for your target buy price; reinvest premium if not assigned

- In the covered call phase: reduce cost basis each cycle; profit from both premium and potential capital gain if called away

- The strategy sacrifices explosive upside for consistent, repeatable income — it is range-bound and sideways-trend friendly

- Target 0.25–0.35 delta CSPs and 0.20–0.30 delta covered calls, both at 30–45 DTE

What’s Next

You’ve now mastered the three core income strategies. Next up, we step into intermediate territory — earnings season. Straddles vs. Strangles: The Earnings Vol Play introduces the directional-neutral strategies that bet on magnitude of movement rather than which way the stock goes.

The wheel works best when you can monitor and roll positions with minimal friction. Tastytrade is purpose-built for exactly this — fast rolling, clear P&L tracking per position, and low per-contract commissions that don’t eat into your premium income cycle after cycle.

Disclosure: this is a referral link. If you sign up via this link, the site may earn a commission at no cost to you.

Disclaimer: This content is for educational and informational purposes only and does not constitute financial, investment, or trading advice. Options trading involves significant risk and is not suitable for all investors. You may lose the entire amount invested. Yield estimates referenced are based on historical options premiums and are not a guarantee of future results. Always conduct your own research and consult a licensed financial advisor before making investment decisions.