Debit Spreads: Directional Bets with Built-In Protection

Debit Spreads: Directional Bets with Built-In Protection

Buying a call option outright is expensive. A 30-delta call on a $170 stock with 30 DTE might cost $4–$6 per share — that’s $400–$600 per contract, all of which can be lost if the stock doesn’t move. And even if the stock moves in your direction, theta decay is eating away at your position every day.

Debit spreads solve both problems. By selling an option at a higher (or lower) strike simultaneously, you offset a significant portion of the premium you pay — reducing your cost, reducing the time decay drag, and defining your maximum risk precisely.

The trade-off: you also cap your upside. But if you have a clear price target in mind, that’s usually an acceptable trade.

Two Types of Debit Spreads

Bull Call Spread (Bullish)

Buy a lower-strike call, sell a higher-strike call at the same expiration. Net debit. Profits if the stock rises to or above the upper strike by expiration.

Bear Put Spread (Bearish)

Buy a higher-strike put, sell a lower-strike put at the same expiration. Net debit. Profits if the stock falls to or below the lower strike by expiration.

The mechanics are mirror images. We’ll focus on the bull call spread here, since the bear put spread is structurally identical in the opposite direction.

Bull Call Spread: The Setup

Example — AAPL at $170, expecting a move toward $180:

Buy 1x AAPL $170 Call (30 DTE) → pay $6.00

Sell 1x AAPL $180 Call (30 DTE) → receive $2.50

─────────────────────────────────────────────────

Net debit paid: $3.50/share = $350/spread

Maximum profit: $6.50/share = $650/spread

Maximum loss: $3.50/share = $350/spreadYou’re paying $3.50 for the right to profit from a move from $170 to $180 — a capped gain of $6.50 per share if the stock hits or exceeds $180 at expiration.

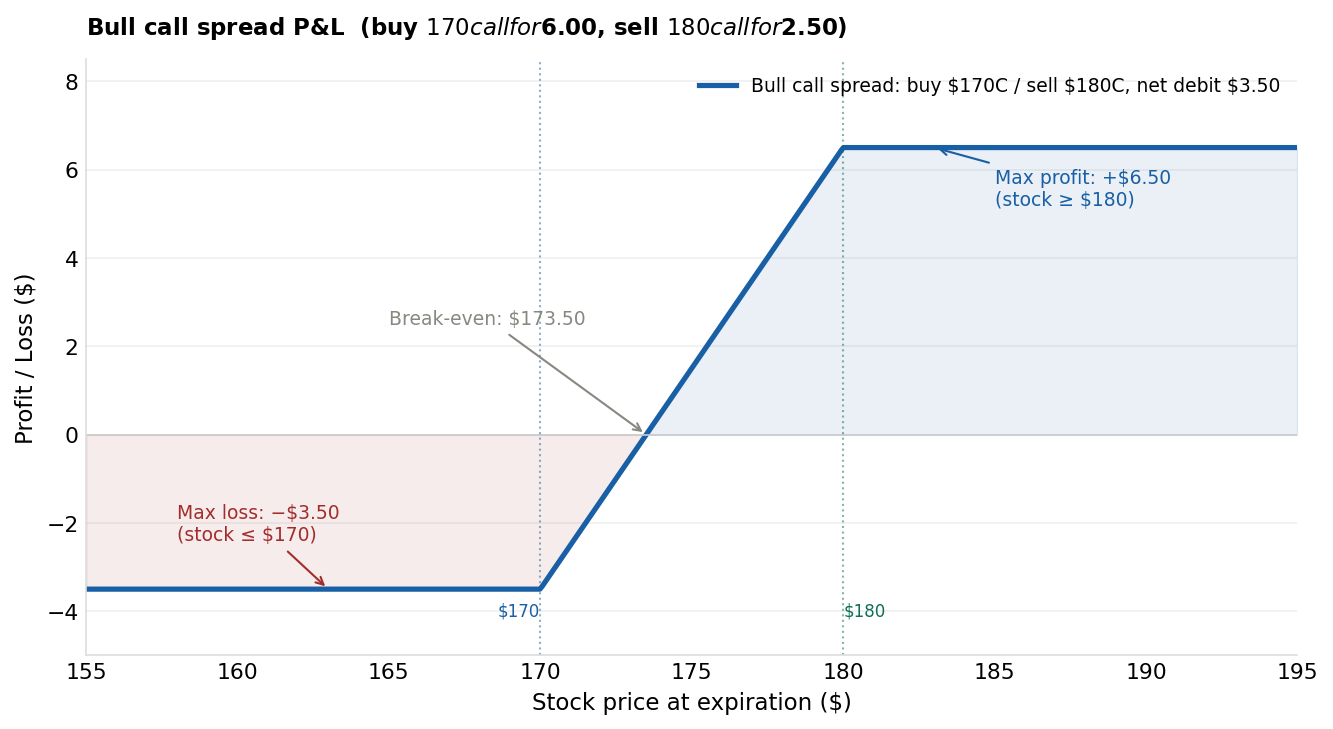

P&L at Expiration

The bull call spread pays max profit ($6.50) if AAPL closes at or above $180. Maximum loss ($3.50) is locked in if AAPL stays at or below $170. Break-even is $173.50.

The bull call spread pays max profit ($6.50) if AAPL closes at or above $180. Maximum loss ($3.50) is locked in if AAPL stays at or below $170. Break-even is $173.50.

Three zones:

Below $170 (max loss zone): Both calls expire worthless. You lose the full $3.50 debit. The short $180 call provided no benefit here — it simply offset some of the premium you paid for the $170 call.

Between $170 and $180 (transition zone): The long $170 call is gaining value but hasn’t reached full intrinsic value. P&L = stock price − $173.50 (the break-even).

Above $180 (max profit zone): Both calls are deep in-the-money. Gains from the $170 call are capped by the short $180 call. Maximum profit = $180 − $170 − $3.50 = $6.50.

Key formulas:

Break-even = Lower strike + Net debit = $170 + $3.50 = $173.50 Max profit = (Upper strike − Lower strike) − Net debit = $10 − $3.50 = $6.50 Max loss = Net debit paid = $3.50 (entire debit if stock closes below lower strike)

Why Debit Spreads Beat Buying Options Outright

Cost reduction: In our example, buying the $170 call outright costs $6.00. The bull call spread costs only $3.50 — a 42% reduction in premium, and therefore a 42% reduction in maximum loss.

Breakeven improvement: An outright $170 call needs AAPL to close above $176 ($170 + $6 premium) just to break even. The spread’s break-even is $173.50 — the stock needs to move $3.50 less.

Reduced theta decay: By selling the $180 call, you collect premium that offsets daily theta erosion. Debit spreads are short theta net — time decay still works against you, since the long leg has more time value than the short leg. The short leg reduces your total theta exposure vs an outright call, but you still lose value each day the stock stays flat.

The trade-off: your upside is capped at $180. If AAPL runs to $200, an outright call would be worth $30 — the spread maxes out at $6.50 regardless.

When to prefer outright options: When you expect a very large, fast move and want uncapped upside. Debit spreads are better when you have a specific price target and want to reduce premium cost.

Credit Spreads vs. Debit Spreads: Which to Use?

This is one of the most common questions at the intermediate level:

| Factor | Credit Spread | Debit Spread |

|---|---|---|

| Premium direction | You receive money | You pay money |

| Profitability driver | Stock doesn’t move much | Stock moves in your favor |

| Directional conviction | Low (range-bound) | High (clear view on direction) |

| Theta position | Long theta (time helps) | Short theta (time hurts) |

| Vega position | Short vega (lower IV helps) | Long vega (higher IV helps) |

| Best IV environment | High IVR → sell spreads | Low IVR → buy spreads |

The practical decision framework:

- Strong directional conviction + low IVR → debit spread

- Range-bound outlook + high IVR → credit spread (see bull put spread or bear call spread)

- No clear view → wait or paper trade

This also means debit spreads pair naturally with elevated stock-specific IV compression (buy a spread after IV has already spiked) or when your technical analysis signals a clear price target within the spread’s structure.

Selecting Strikes for a Bull Call Spread

Long (lower) strike: Choose ATM or slightly OTM. Buying ATM gives you maximum delta sensitivity — the position moves most closely with the stock. Buying OTM reduces cost but also reduces probability and delta, making the trade harder to profit from.

Short (upper) strike: Set near your price target. If you expect AAPL to move from $170 to $180, sell the $180 call. This captures your target move fully while reducing premium cost.

Spread width: Wider spreads ($10) have higher max profit but also higher cost. Narrower spreads ($5) cost less and have a lower break-even, but max profit is limited. Choose width based on your price target and risk tolerance.

Risk/reward target: Many traders require a minimum 1:1.5 or 1:2 risk/reward on debit spreads — i.e., max profit should be at least 1.5× the max loss.

In our example: risk = $3.50, reward = $6.50. That’s a 1:1.86 ratio — acceptable.

Managing Debit Spreads

At max profit (short strike reached): You can close the spread to lock in gains, or hold briefly to see if the stock extends (at the risk of a reversal). Closing at 75–80% of max profit is a disciplined approach.

At a 50% loss: If the spread has lost half its value and your thesis hasn’t played out, close it. Taking a 50% debit loss ($1.75 on a $3.50 debit) is significantly better than riding to zero.

Rolling debit spreads: If the stock hasn’t moved enough but your thesis is intact, you can roll out in time by closing the current spread and reopening the same structure in the next expiration. This extends the trade but adds more premium cost.

Bear Put Spread: The Mirror Image

For bearish setups, the same logic applies:

Buy 1x AAPL $170 Put (30 DTE) → pay $5.50

Sell 1x AAPL $160 Put (30 DTE) → receive $2.00

─────────────────────────────────────────────────

Net debit: $3.50

Break-even: $170 − $3.50 = $166.50

Max profit: $10 − $3.50 = $6.50 (stock at or below $160)

Max loss: $3.50 (stock at or above $170)Same structure, opposite direction. Use when you expect a meaningful move lower, have a specific downside target, and want to reduce the premium cost of a long put.

Key Takeaways

- A bull call spread = buy lower-strike call + sell higher-strike call (net debit); profits when stock rises

- A bear put spread = buy higher-strike put + sell lower-strike put (net debit); profits when stock falls

- Max profit = spread width − net debit (capped at upper/lower strike)

- Max loss = net debit paid (both legs expire worthless against you)

- Debit spreads cost less than outright options and have a tighter break-even — at the cost of capped upside

- Best in low-to-moderate IVR when you have clear directional conviction and a specific price target

- Require a minimum 1:1.5 risk/reward ratio to be worth trading

What’s Next

Debit and credit spreads trade time-to-expiration in a straight line. Calendar spreads trade it on two different axes simultaneously. Calendar Spreads: Harvesting Time Across Expirations introduces the strategy that monetizes the difference in theta decay rates between near-term and far-term options.

For executing debit spreads as a single order with a defined max risk, Tastytrade makes it straightforward — their order ticket calculates the net debit, max profit at expiration, and break-even price automatically so you can evaluate the trade before committing capital.

Disclosure: this is a referral link. If you sign up via this link, the site may earn a commission at no cost to you.

Disclaimer: This content is for educational and informational purposes only and does not constitute financial, investment, or trading advice. Options trading involves significant risk and is not suitable for all investors. You may lose the entire amount invested. Always conduct your own research and consult a licensed financial advisor before making investment decisions.