The Poor Man's Covered Call: LEAPS as a Stock Substitute

The Poor Man’s Covered Call: LEAPS as a Stock Substitute

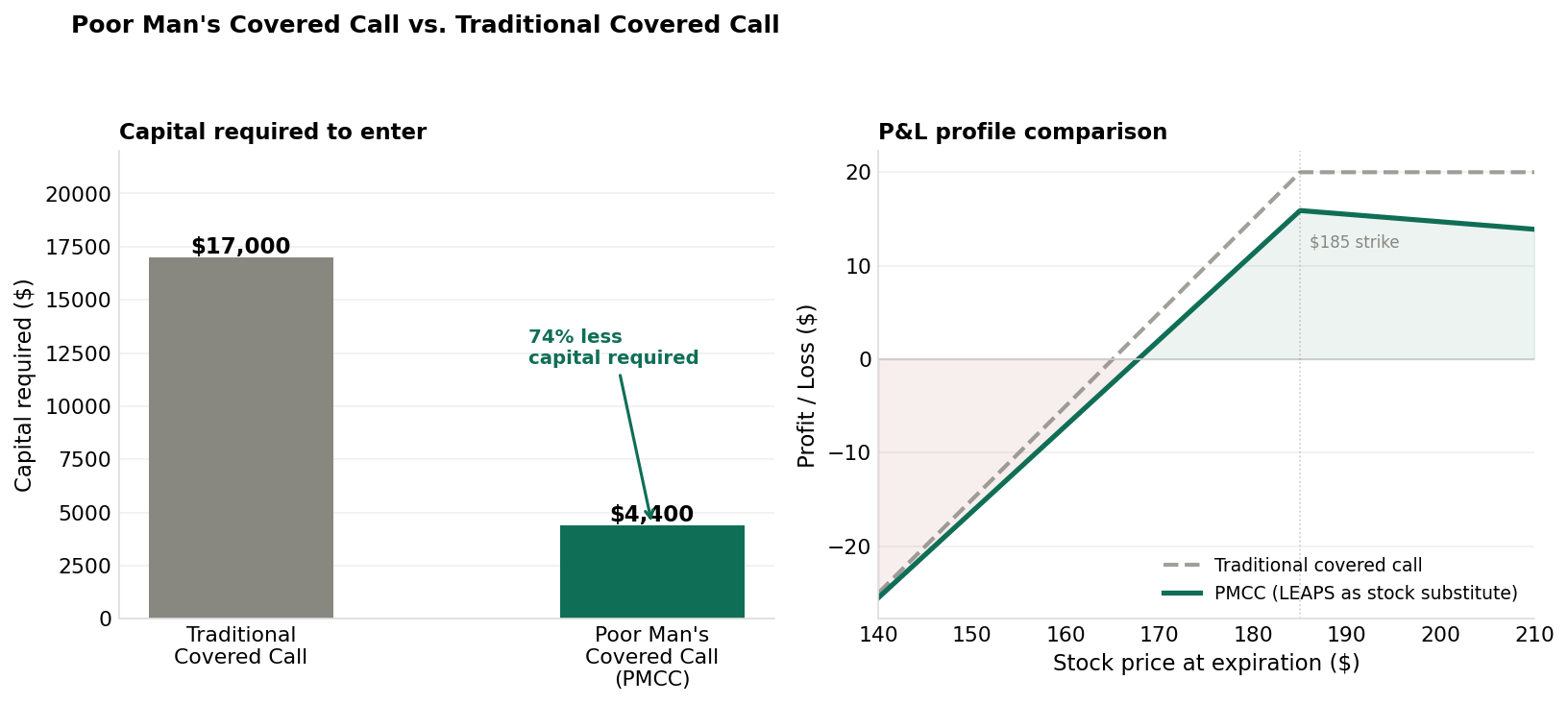

A traditional covered call on AAPL requires owning 100 shares — roughly $17,000 in capital. For many traders, that’s a significant portion of an account tied up in a single position. The strategy works great, but the capital requirement limits how many positions you can run and how diversified you can be.

The Poor Man’s Covered Call (PMCC) solves this elegantly. Instead of buying 100 shares, you buy a deep in-the-money LEAPS call option that behaves almost like the stock — at a fraction of the cost. Then you sell near-term OTM calls against it exactly as you would in a traditional covered call.

The result: similar income profile, similar directional exposure, roughly 75% less capital required.

What Is a LEAPS Option?

LEAPS stands for Long-Term Equity Anticipation Securities. These are options contracts with expirations more than 12 months in the future — typically 1 to 3 years out.

A deep in-the-money LEAPS call (delta of 0.75–0.85) behaves very similarly to owning shares because:

- It has high intrinsic value and relatively little time value compared to its total price

- Its delta means it moves approximately $0.80 for every $1 the stock moves

- It has low gamma, so its delta stays relatively stable over time

This is why a deep ITM LEAPS call is often called a “stock substitute” — it captures most of the stock’s directional movement at a fraction of the purchase price.

PMCC Setup: The Full Structure

Example — AAPL at $170, 12 months out:

LEAPS (long leg — replaces stock):

Buy 1x AAPL $130 Call, 12 months (Jan LEAPS) → pay $43.00

Delta: ~0.82 | Capital required: $4,300

Short call (income leg — identical to standard covered call):

Sell 1x AAPL $185 Call, 30 DTE → receive $3.00

Net position cost (LEAPS purchase − short call credit):

$43.00 − $3.00 = $40.00 effective cost per share = $4,000 netCompare to traditional covered call: $17,000 for 100 shares + short $185 call.

Capital Efficiency and Return Comparison

Left: The PMCC requires ~74% less capital than a traditional covered call. Right: The P&L profiles are similar in shape — the PMCC retains upside slightly better per dollar invested, but diverges at very low stock prices due to LEAPS value decay.

Left: The PMCC requires ~74% less capital than a traditional covered call. Right: The P&L profiles are similar in shape — the PMCC retains upside slightly better per dollar invested, but diverges at very low stock prices due to LEAPS value decay.

Capital comparison:

| Approach | Capital Required | Monthly Income | Return on Capital |

|---|---|---|---|

| Traditional CC (100 shares @ $170) | $17,000 | $300/month | 1.8%/month |

| PMCC (LEAPS @ $43) | $4,300 | $240–$300/month | 5.6–7%/month |

The PMCC’s return on capital is substantially higher because you’re deploying less capital for a similar income stream. This is why active traders often prefer the PMCC for capital efficiency.

The Key Constraint: LEAPS Strike Must Be Below Short Call Strike

This is the critical rule that many PMCC traders overlook:

The LEAPS (long call) strike must always be below the short call strike.

In our example: LEAPS strike is $130, short call is $185. There’s $55 of buffer. This ensures that if the short call is exercised (AAPL surges above $185), you can always exercise your LEAPS to deliver shares — or simply close both legs.

What happens if short call is exercised?

- You don’t own shares — you can’t deliver them directly

- You close the short call at a loss, then sell the LEAPS for a profit to offset

- Or you exercise the LEAPS (buy shares at $130) and sell shares at $185 — a $55 gain that offsets costs

This process is messier than a traditional covered call assignment (where you simply deliver your shares), which is why you should manage the PMCC actively and avoid letting the short call go deep ITM.

Selecting the LEAPS: What to Look For

Delta: Target 0.75–0.85 delta. This gives you near-stock-like exposure without paying full stock price. Lower delta = cheaper LEAPS but less stock-like behavior and more time-value decay risk.

DTE: At least 12 months (365+ days), preferably 18–24 months. Longer DTE means slower LEAPS decay, giving you more time to collect covered call income before the LEAPS needs to be rolled.

Strike: As a rule, buy the LEAPS strike that puts you at least 20–25 points below the current stock price for a $170 stock. Deep ITM keeps delta high and minimizes time-value waste.

Selling the Short Calls: Same as a Covered Call

The short call leg of a PMCC is managed identically to a standard covered call:

- Strike: 0.20–0.30 delta, OTM (above both the current stock price and — critically — always above the LEAPS strike)

- DTE: 30–45 days to expiration

- Close at: 50% of premium collected (~21 DTE)

- Roll if tested: Roll up-and-out if the stock approaches the short call strike

The only difference from a traditional covered call: you cannot let the short call go deep ITM without risk, because you don’t hold shares to deliver. Stay active on management.

The LEAPS Roll: Maintaining the Position

LEAPS options have expiration dates like any other option. As the LEAPS approaches its expiration (typically when it has 3–6 months remaining), you need to roll it forward:

- Sell the existing LEAPS (still has significant intrinsic value)

- Buy a new LEAPS with 12–18+ months remaining at the same or similar strike

- Net cost of roll = new LEAPS price − proceeds from selling old LEAPS

If the stock has risen since you bought the LEAPS, the roll often produces a credit or at minimal cost. If the stock has fallen significantly, the roll may cost more — reducing returns.

Risks Specific to the PMCC

LEAPS time value decay: Even a deep ITM LEAPS loses time value as it approaches expiration. This is slower than short-dated options but real — it’s one reason PMCC returns slightly underperform traditional covered calls in flat-to-sideways markets (the LEAPS decays while you collect short-call premium).

Gap risk: A sharp stock decline doesn’t just reduce the LEAPS’ intrinsic value — it also reduces its delta, meaning it recovers more slowly than shares would. At extreme down moves, the LEAPS value collapse can exceed what short call premium you’ve collected.

Leverage risk: The PMCC provides more leverage per dollar than owning shares. This magnifies both gains and losses as a percentage of capital deployed.

Assignment complexity: If the short call is exercised before you manage it, the mechanics require immediate action. Set alerts when the stock approaches your short call strike.

Is the PMCC Right for You?

The PMCC is best for traders who:

- Understand covered calls well and want more capital efficiency

- Are comfortable with the additional complexity of managing a LEAPS roll

- Want to run multiple income positions without concentrating all capital in large stock positions

- Are trading in accounts where buying stock outright is impractical (some options-only accounts or smaller accounts)

It’s not ideal for beginners — the assignment mechanics, LEAPS rolls, and active management requirements make it intermediate-to-advanced territory.

Key Takeaways

- A PMCC = deep ITM LEAPS call (long leg) + short near-term OTM call (income leg)

- The LEAPS replaces 100 shares of stock at roughly 20–30% of the capital cost

- LEAPS strike must always be below the short call strike — this is non-negotiable

- Target LEAPS with 0.75–0.85 delta, 12–24 months DTE; roll when 3–6 months remain

- Short call management is identical to a standard covered call: 0.20–0.30 delta, 30–45 DTE, close at 50%

- Returns on capital are substantially higher than traditional covered calls — but so are complexity and leverage

What’s Next

You now have a full toolkit of strategies. The next skill is what separates traders who survive from those who don’t: knowing how to adjust when a position moves against you. Rolling Options: How to Adjust Positions That Go Against You covers the mechanics and decision framework for keeping positions alive — and knowing when to just close them.

The PMCC involves holding a long LEAPS while repeatedly selling short-term calls — a workflow that’s much smoother on a platform built for active options traders. Tastytrade tracks your net cost basis across the full position and makes it easy to roll the short leg each cycle without disturbing your LEAPS.

Disclosure: this is a referral link. If you sign up via this link, the site may earn a commission at no cost to you.

Disclaimer: This content is for educational and informational purposes only and does not constitute financial, investment, or trading advice. Options trading involves significant risk and is not suitable for all investors. You may lose the entire amount invested. Always conduct your own research and consult a licensed financial advisor before making investment decisions.