Bull Put Spreads: Defined-Risk Income on Your Own Terms

Bull Put Spreads: Defined-Risk Income on Your Own Terms

The cash-secured put is a great strategy — until your broker shows you the margin requirement. Selling a put on a $170 stock means having $16,500 reserved per contract just in case you’re assigned. For many traders, that’s most of a small account.

The bull put spread solves this problem. It’s the cash-secured put’s tighter, more capital-efficient cousin: same bullish-to-neutral thesis, same premium income, but with a built-in safety net that caps your maximum loss — and dramatically reduces the capital required.

The Mechanics: Two Legs, One Trade

A bull put spread (also called a short put spread or put credit spread) involves two simultaneous options trades:

- Sell an OTM put at a higher strike — this is your income-generating leg

- Buy a further OTM put at a lower strike — this is your protection leg, which caps your downside

You collect premium from the short put and pay a smaller amount for the long put. The difference is your net credit — the maximum you can earn on the trade.

Example setup — AAPL at $170:

Sell 1x AAPL $165 Put (30 DTE) → receive $3.50

Buy 1x AAPL $160 Put (30 DTE) → pay $1.00

─────────────────────────────────────────────────

Net credit received: $2.50/share = $250/spread

Maximum risk: $2.50/share = $250/spread

Capital required: $250 (vs $16,500 for naked CSP)P&L at Expiration

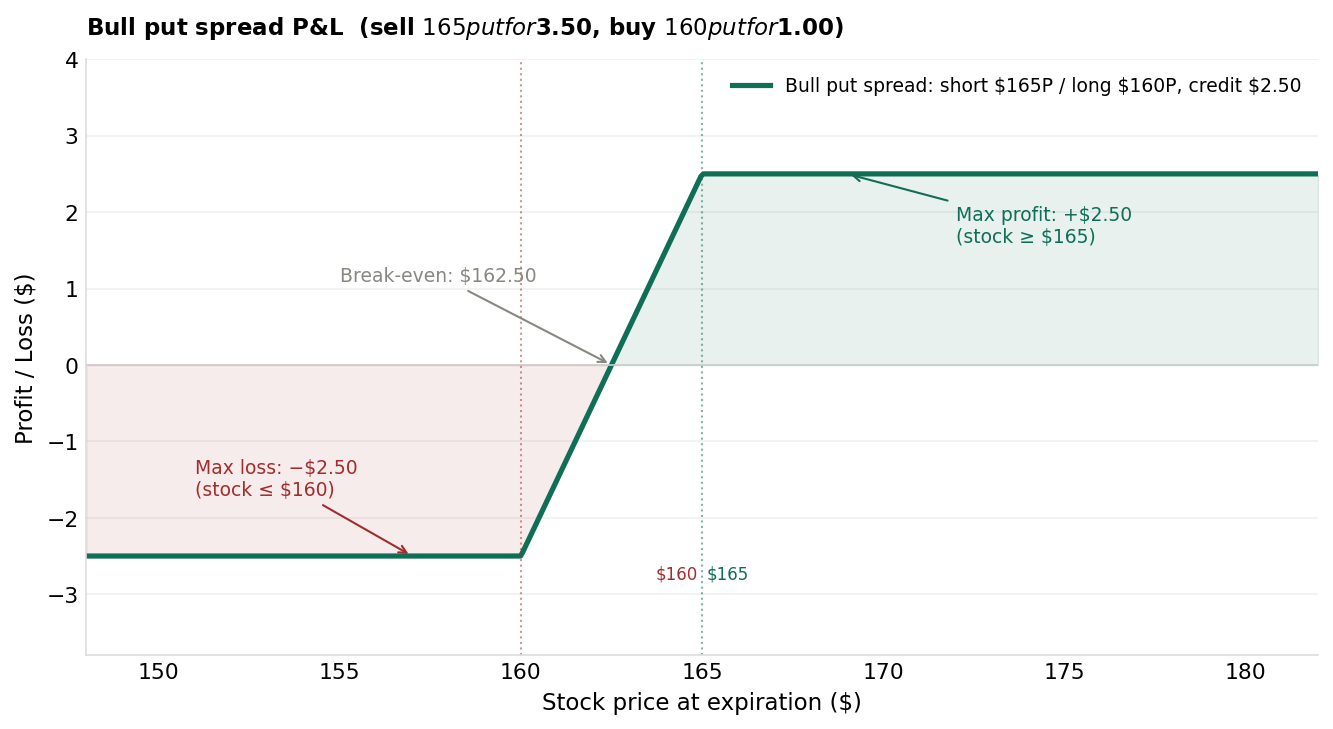

The bull put spread delivers max profit ($2.50) if AAPL closes above $165. Below $160, the max loss is capped at $2.50. Break-even is $162.50.

The bull put spread delivers max profit ($2.50) if AAPL closes above $165. Below $160, the max loss is capped at $2.50. Break-even is $162.50.

Three zones to understand:

Above $165 (max profit zone): Both puts expire worthless. You keep the full $2.50 net credit. This is the ideal outcome.

Between $160 and $165 (transition zone): The short $165 put is in-the-money, but the long $160 put partially offsets the loss. P&L = stock price − $162.50 (break-even). This zone produces partial losses ranging from $0 to −$2.50.

Below $160 (max loss zone): Both puts are deep in-the-money. The loss on the short $165 put is fully offset by the gain on the long $160 put — except for the net spread width ($5) minus the credit received ($2.50). Maximum loss is capped at exactly $2.50/share = $250 per spread.

Key formulas:

Break-even = Short strike − Net credit = $165 − $2.50 = $162.50 Max profit = Net credit received = $2.50 ($250 per contract) Max loss = Spread width − Net credit = $5 − $2.50 = $2.50 ($250 per contract)

Why Spreads Beat Naked Puts on Capital Efficiency

The key metric for income trades is return on capital (ROC) — how much you earn relative to what you have at risk.

| Trade | Premium | Capital Required | Max Loss | ROC |

|---|---|---|---|---|

| Cash-secured put ($165P) | $400 | $16,500 | $16,100 | 2.4% |

| Bull put spread ($160/$165) | $250 | $250 | $250 | 100% |

A bull put spread’s ROC is dramatically higher because your maximum risk equals your maximum gain in this example (a 50% credit/width ratio — you received half the spread width as credit). In practice, selling a 0.25–0.35 delta put spread typically delivers 20–35% ROC, not 100% — still far superior to a CSP, without exaggerating. The trade-off: if you’re assigned on a CSP, you own shares you can wheel. With a spread, assignment is more complex and typically avoided.

For traders deploying capital across many positions, spreads allow far more diversification with the same account size.

Strike Selection and Trade Setup

The same delta-based framework from covered calls applies here:

Short put (sold leg): Target the 0.25–0.35 delta OTM put. This provides meaningful premium while keeping a 65–75% probability of expiring worthless.

Long put (buying leg): Choose a strike $5–$10 below the short strike. Wider spreads have larger max loss but more protection from tail moves. Narrower spreads (e.g., $2.50 wide) have lower max loss but less premium per dollar of risk.

Expiration: Same 30–45 DTE framework as all premium-selling strategies. Close at 50% profit (~21 DTE) and redeploy.

When the Bull Put Spread Shines

The setup works best when:

- IV is elevated — you collect more premium per unit of risk in high-IV environments

- The stock has strong support near your short strike — technical levels add conviction to the probability thesis

- You want income without concentration risk — spreads let you run multiple positions across sectors without overcommitting capital

The strategy struggles in sharp, rapid downturns where the stock blows through both strikes. Unlike owning shares (where losses are unrealized), both spread legs settle in cash at expiration — the max loss is realized.

Managing the Trade

At 50% profit (target exit): Buy back the spread for half the credit received. Example: sold for $2.50, close for $1.25. Bank $1.25 profit, move to the next cycle.

If the stock approaches the short strike with >21 DTE: Consider rolling the spread down-and-out — buy back the current spread and sell a new spread at a lower strike in the next expiration for a credit. This extends your runway without adding to your loss.

At max loss (stock below both strikes with <5 DTE): Let the spread expire. Do NOT add to a losing position to “lower your average.” Both legs will settle automatically; you’ll receive the net loss in your account.

Bull Put Spread vs. Cash-Secured Put: Which to Use?

| Factor | Bull Put Spread | Cash-Secured Put |

|---|---|---|

| Capital required | Low (spread width) | High (strike × 100) |

| Max profit | Net credit only | Net credit only |

| Max loss | Capped (spread width − credit) | Large (effective cost basis) |

| Assignment outcome | Rare/complex | Normal — you own shares |

| Best for | Multiple positions, small accounts | Wheels, stock acquisition strategy |

| IV preference | High IV | High IV |

Rule of thumb: Use CSPs when you genuinely want to own the underlying stock and plan to wheel. Use bull put spreads when you want income without the capital commitment or the intent to hold shares.

Key Takeaways

- A bull put spread = sell higher-strike put + buy lower-strike put at the same expiration; both OTM

- Net credit = max profit, collected if the stock stays above the short strike at expiration

- Max loss = spread width − net credit — fully capped regardless of how far the stock falls

- Capital required equals only the maximum loss — dramatically more efficient than a cash-secured put

- Target 0.25–0.35 delta short put, 30–45 DTE; close at 50% of credit received

- Use when you want premium income without capital-heavy stock ownership commitment

What’s Next

You’ve got the put credit spread. Now let’s look at its mirror image on the call side: Bear Call Spreads: The Bearish Income Play — the same mechanics, applied when you expect a stock to stay flat or decline.

To trade bull put spreads with a platform built for multi-leg options, check out Tastytrade — they offer low per-contract commissions with no leg-by-leg fees on spreads, and their order ticket shows your max profit, max loss, and probability of profit before you submit.

Disclosure: this is a referral link. If you sign up via this link, the site may earn a commission at no cost to you.

Disclaimer: This content is for educational and informational purposes only and does not constitute financial, investment, or trading advice. Options trading involves significant risk and is not suitable for all investors. You may lose the entire amount invested. Always conduct your own research and consult a licensed financial advisor before making investment decisions.