Bear Call Spreads: Collect Premium When a Stock Is Stalling

Bear Call Spreads: Collect Premium When a Stock Is Stalling

Not every trade is a bullish bet. Sometimes a stock is extended, hitting resistance, or simply grinding sideways in a range where you don’t want to own it — but you still want to extract income from it. That’s where the bear call spread comes in.

The bear call spread is the structural mirror image of the bull put spread: a two-leg options credit trade with defined risk on the upside, a bearish-to-neutral bias, and no requirement to own shares. It’s one of the most underused income tools for traders who spend all their time on the put side.

The Mechanics

A bear call spread (also called a short call spread or call credit spread) involves:

- Sell an OTM call at a lower strike — your income leg

- Buy a further OTM call at a higher strike — your protection leg, which caps your upside risk

The net credit you collect is your maximum profit. The spread width minus that credit is your maximum loss.

Example setup — AAPL at $170, approaching resistance at $175:

Sell 1x AAPL $175 Call (30 DTE) → receive $3.50

Buy 1x AAPL $180 Call (30 DTE) → pay $1.00

─────────────────────────────────────────────────

Net credit received: $2.50/share = $250/spread

Maximum loss: $2.50/share = $250/spread

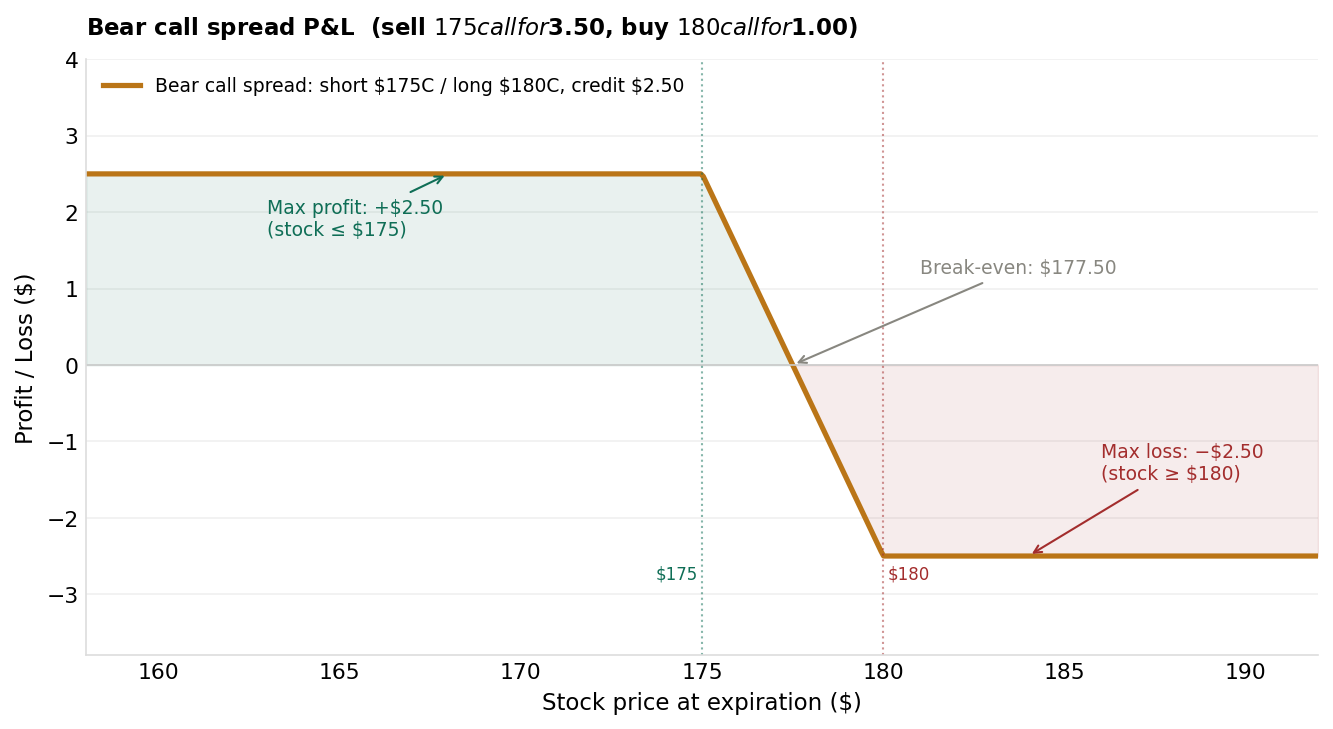

Capital required: $250 margin holdP&L at Expiration

The bear call spread earns max profit ($2.50) if AAPL stays below $175. Above $180, the loss is capped at $2.50. Break-even is $177.50.

The bear call spread earns max profit ($2.50) if AAPL stays below $175. Above $180, the loss is capped at $2.50. Break-even is $177.50.

Three zones:

Below $175 (max profit zone): Both calls expire worthless. You keep the full $2.50 credit.

Between $175 and $180 (transition zone): The short call is in-the-money, but the long $180 call offsets the loss. P&L = $177.50 − stock price (break-even line).

Above $180 (max loss zone): Both calls are deep in-the-money. The long $180 call fully offsets losses above $180, leaving you with exactly −$2.50/share = −$250 per spread.

Key formulas:

Break-even = Short strike + Net credit = $175 + $2.50 = $177.50 Max profit = Net credit = $2.50 ($250 per contract) Max loss = Spread width − Net credit = $5 − $2.50 = $2.50 ($250 per contract)

When to Use a Bear Call Spread

The bear call spread works best in these conditions:

Neutral to mildly bearish environment: You don’t need the stock to fall — you just need it not to rise significantly above your short call strike by expiration. The stock can move sideways or drift slightly lower and you win.

Elevated implied volatility: As with all premium-selling trades, high IV means richer premiums. You collect more credit for the same risk.

Technical resistance nearby: If a stock has been rejected at $175 three times in the past month, selling a $175 call has both statistical and technical support. Spreads pair well with chart analysis.

Earnings avoidance: If a stock has already reported earnings and IV is compressing back to baseline, selling an OTM call spread with declining IV tailwind can be highly efficient.

Comparing the Two Credit Spreads

| Feature | Bull Put Spread | Bear Call Spread |

|---|---|---|

| Direction | Neutral-to-bullish | Neutral-to-bearish |

| Legs | Sell higher-strike put + buy lower-strike put | Sell lower-strike call + buy higher-strike call |

| Profits when… | Stock stays above short strike | Stock stays below short strike |

| Loses when… | Stock falls below both strikes | Stock rises above both strikes |

| Capital at risk | Spread width − credit | Spread width − credit |

| Requires owning shares? | No | No |

The math is identical — only the direction changes. This symmetry is why the two are often combined into a single position: the iron condor.

Strike Selection

The same 0.25–0.35 delta framework applies to the short call leg:

Target the short call at the 0.20–0.30 delta strike — one notch lower than the 0.25–0.35 range used for short puts. The reason is volatility skew: OTM puts carry higher implied volatility than OTM calls at the same delta, because market demand for downside protection inflates put premiums. On the call side, 0.20–0.30 delta typically yields comparable premium to a 0.25–0.35 delta put. At this delta, there’s approximately a 70–80% probability the stock closes below that strike at expiration. For a $170 stock with 30 DTE and moderate volatility, this typically puts the short call at $175–$180.

Width of spread: A $5 spread is standard. Wider spreads ($10) give more max loss protection in exchange for higher potential loss — useful if you want to sell a tighter delta for more premium. Narrower spreads ($2.50) reduce max loss and max gain proportionally.

Avoid selling calls below key technical levels. If the stock is clearly breaking out above resistance, don’t sell a call spread against the momentum. Spreads work with mean-reversion, not against trends.

Bear Call Spreads vs. Covered Calls

If you already own shares of the stock, a covered call achieves a similar effect (capped upside, premium income) without needing to commit additional margin. The covered call has no max loss on the downside (the stock itself carries that risk), while the bear call spread does.

Use a bear call spread when:

- You don’t own the underlying shares

- You want defined risk on a specific range

- You want to trade bearish-to-neutral on a stock you wouldn’t want to own

Use a covered call when:

- You own 100 shares and want to generate income from them

- You’re comfortable holding shares through a correction

- You’re executing a wheel strategy

Managing Bear Call Spreads

At 50% profit: Close the spread. Buy back the short $175 call and sell the long $180 call simultaneously for a net debit of roughly $1.25. Pocket $1.25 profit and move on.

If the stock is approaching your short call (danger zone):

Option A: Roll the spread up and out. Close the current $175/$180 spread and open a $178/$183 spread in the next expiration cycle for a net credit. You give yourself more runway and more buffer.

Option B: Close for a small loss. If you’ve already captured 50-60% of the potential max loss on the trade, closing early and redeploying into a fresh, better-positioned spread is often better than rolling.

Never short additional naked calls to “average up.” Bear call spreads have defined risk — that’s the point. Don’t violate it by adding uncovered exposure.

The IVR Connection

Bear call spreads, like all credit spreads, perform better when entered in elevated volatility environments (IV Rank above 40–50%). In low-IV markets, premiums shrink and the risk/reward becomes less attractive.

A quick check before entering any credit spread: pull up the stock’s IV rank. If IVR is below 20%, consider waiting for a better entry or reducing position size. We cover this in detail in IV Rank and IV Percentile: Timing Your Premium Sales.

Key Takeaways

- A bear call spread = sell lower-strike OTM call + buy higher-strike OTM call at the same expiration

- Max profit = net credit received (if stock stays below the short call strike at expiration)

- Max loss = spread width − net credit (fully capped if stock surges above both strikes)

- Best in neutral-to-bearish setups with elevated IV and clear resistance above the short strike

- Target 0.20–0.30 delta short call, 30–45 DTE; close at 50% credit received

- Pairs naturally with a bull put spread to form an iron condor on the same underlying

What’s Next

Two credit spreads. Two directions. Now combine them: The Iron Condor: Four Legs, One Income Trade — the definitive range-bound premium-selling strategy that puts both spreads to work simultaneously.

Tastytrade is the platform of choice for credit spread traders — their interface lets you place bear call spreads as a single two-leg order, see the net credit upfront, and monitor your defined-risk position in one clean P&L view.

Disclosure: this is a referral link. If you sign up via this link, the site may earn a commission at no cost to you.

Disclaimer: This content is for educational and informational purposes only and does not constitute financial, investment, or trading advice. Options trading involves significant risk and is not suitable for all investors. You may lose the entire amount invested. Always conduct your own research and consult a licensed financial advisor before making investment decisions.