Position Sizing and Portfolio Risk: The Framework Pro Traders Use

Position Sizing and Portfolio Risk: The Framework Pro Traders Use

Trading skill without position sizing is an engine without a governor. You can be right 80% of the time, use every strategy in this blog correctly, and still blow up your account if one oversized position goes catastrophically wrong. Conversely, a trader with average strategy selection and excellent position sizing will outperform a skilled trader with poor risk management over any sufficiently long timeframe.

This is the article that makes everything else sustainable.

The Core Principle: Risk a Fixed Percentage Per Trade

Professional traders don’t think in dollar amounts per trade — they think in percentages of their total portfolio. This creates consistency: when the account grows, position sizes scale up proportionally; when the account shrinks after losses, position sizes automatically scale down.

The Options Seller’s Rule: Risk no more than 2–5% of your total account on any single trade.

“Risk” means your maximum possible loss on the trade — not the premium you collect, not the notional value, not the margin required. The maximum loss.

Example for a $50,000 account:

- 2% max risk per trade = $1,000 maximum loss

- 5% max risk per trade = $2,500 maximum loss

A bull put spread with a $2.50 max loss per share:

- At 2% risk on $50K: $1,000 ÷ $250 per spread = 4 spreads maximum

- At 5% risk on $50K: $2,500 ÷ $250 per spread = 10 spreads maximum

Not All “2%” Is Equal: Risk vs. Capital

A common confusion: for a cash-secured put, is the “2% risk” based on the maximum loss or the total capital committed?

Use maximum loss (defined risk), not total capital committed.

A CSP on a $165 stock commits $16,500 in capital but has a maximum defined loss much lower (the effective cost basis minus zero, but typically risk-managed at 2× the premium). For sizing purposes, treat the maximum anticipated loss as your risk figure.

For undefined-risk positions (naked puts, uncovered calls): the position’s theoretical maximum loss is very large. Professional traders typically limit these to 1–2% of portfolio AND also limit total portfolio delta exposure (see below). If you’re not on portfolio margin and trading naked options, your broker’s margin requirement provides a natural sizing limit — but don’t treat margin as your risk limit.

Portfolio-Level Thinking: The Bigger Picture

Individual position sizing is necessary but not sufficient. A portfolio of 10 independent, properly-sized positions can still have dangerous aggregate risk if all 10 positions move together.

Portfolio Delta: Your Net Market Exposure

Delta at the portfolio level tells you how much your total portfolio moves per $1 move in the broader market (or per $1 move in a correlated basket of stocks).

If you run eight bullish trades (positive delta) and no bearish or neutral trades, your portfolio is long the market. A sharp sell-off hits all eight simultaneously.

Monitoring portfolio delta:

- Sum the delta of all positions, adjusted for shares (×100 per contract)

- A well-diversified income portfolio typically runs near-zero net delta

- Set a personal limit: e.g., “Portfolio delta never exceeds ±500” (equivalent to being long/short 500 shares of the S&P 500)

Portfolio Theta: Your Daily Income

Portfolio theta is your daily income from all premium-selling positions combined. Professional premium sellers often size to achieve a target daily theta — say, 0.1–0.2% of portfolio value per day.

For a $50,000 portfolio:

- Target: 0.1–0.15% daily theta = $50–$75/day from all positions combined

- This represents roughly 1.5–2.5% per month in theoretical income before losses

Portfolio Vega: Your IV Exposure

Portfolio vega measures how much your account value changes per 1% change in implied volatility.

If all your positions are short vega (iron condors, short strangles, credit spreads), a VIX spike from 18 to 30 will show significant paper losses across the board. Balancing short-vega positions with some long-vega exposure (calendars, long options as hedges) smooths out volatility-driven P&L swings.

Position Sizing by Portfolio Tier

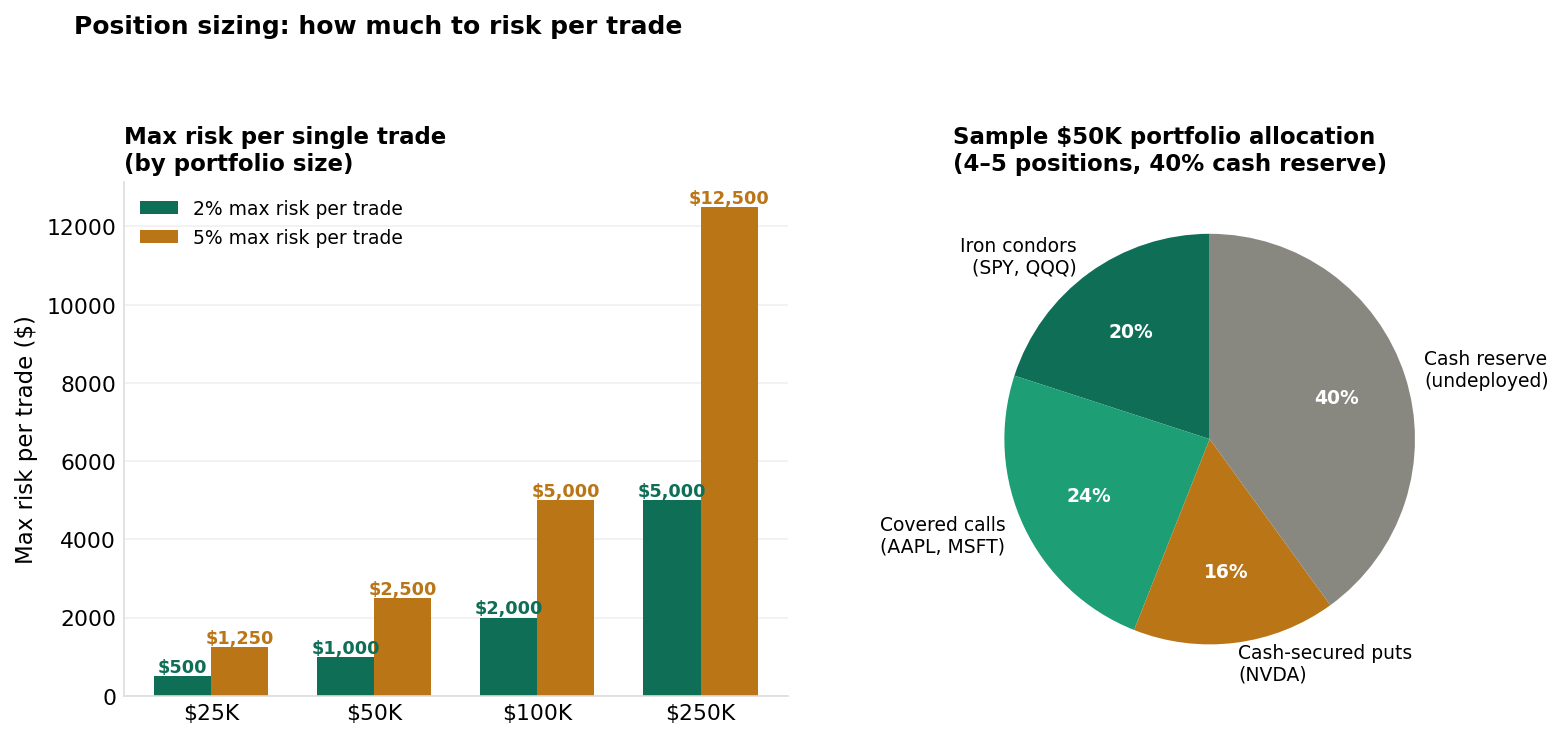

Left: max risk per trade scales linearly with portfolio size. Right: a sample $50K portfolio allocation showing 4–5 positions with 40% cash reserve.

Left: max risk per trade scales linearly with portfolio size. Right: a sample $50K portfolio allocation showing 4–5 positions with 40% cash reserve.

Practical sizing guidelines by account size:

| Account Size | Max Risk Per Trade (2%) | Max Risk Per Trade (5%) | Target Positions | Cash Reserve |

|---|---|---|---|---|

| $10,000 | $200 | $500 | 3–4 | 30–40% |

| $25,000 | $500 | $1,250 | 4–6 | 30–40% |

| $50,000 | $1,000 | $2,500 | 6–10 | 25–35% |

| $100,000 | $2,000 | $5,000 | 8–15 | 20–30% |

| $250,000+ | $5,000 | $12,500 | 12–20 | 15–25% |

Why keep a cash reserve? Markets occasionally provide exceptional opportunities — a spike in VIX, a sector sell-off that inflates put premiums, or an unusual situation where spreads are priced very attractively. Keeping 20–40% in cash means you can act on these opportunities without closing existing positions.

Correlation: The Hidden Risk Multiplier

Two positions that seem independent can actually be highly correlated. AAPL and QQQ both fall when tech sells off. NVDA and AMD move together. JPM and BAC are correlated by sector. Owning “10 different positions” across 10 different stocks doesn’t mean you have 10 independent risk units if all 10 are tech-sector earnings-dependent.

Practical correlation management:

- Spread positions across uncorrelated sectors (tech, financials, energy, consumer staples)

- Include at least one position in a broad index (SPY, QQQ, IWM) — these tend to be more mean-reverting than individual stocks

- Limit exposure to any single sector to 25–30% of total positions

- Be cautious about holding more than 2–3 positions that all face earnings in the same week

The 50% Rule: Never Lose More Than Half Your Profits First

Here’s a portfolio-level rule used by many professional traders: if your portfolio is down more than 50% of the prior month’s gains in the current month, stop entering new positions and focus on managing existing ones.

If you made $2,000 in January and you’re down $1,000 in February, something is wrong with your positioning or the market environment. Pausing and evaluating is smarter than doubling down.

Similarly: if you’ve had 3 consecutive losing months, reduce position sizes by 25–50% until you rebuild confidence and the market regime becomes clearer.

A Simple Portfolio Management Routine

Weekly check (5 minutes):

- Review each position: P&L vs. plan, DTE remaining

- Close any position at 50% profit target or loss limit

- Check portfolio-level delta: is it near-neutral?

- Check total capital at risk: does it fit within your sizing rules?

Monthly review (15–30 minutes):

- Total P&L: theta earned vs. losses taken

- Win rate and average gain/loss per trade

- Were position sizing rules followed consistently?

- What’s the next month’s IV environment looking like? (IVR across your trading universe)

- Are upcoming earnings events affecting any current or planned positions?

The Compound Effect of Good Sizing

Here’s why position sizing is the highest-leverage skill in your toolkit:

A trader who risks 10% per trade and hits a 5-trade losing streak (possible, even with a 70% win rate) suffers a 41% drawdown: (0.90)^5 = 0.59. Recovering from a 41% loss requires a 70% gain just to break even.

A trader who risks 2% per trade and hits the same 5-trade losing streak suffers a 10% drawdown: (0.98)^5 = 0.90. They need only an 11% gain to recover.

Same strategy. Same losing streak. Vastly different outcomes. Position sizing is not defensive — it’s mathematically the most aggressive thing you can do for long-term account growth.

Key Takeaways

- Risk 2–5% of total portfolio value per trade, measured by maximum defined loss — not premium, not margin

- Monitor portfolio-level Greeks: keep net delta near-neutral, target a daily theta of 0.1–0.2% of portfolio, watch for excessive short-vega clustering

- Maintain a 20–40% cash reserve at all times for opportunistic trades and emergency management

- Manage correlation: diversify across uncorrelated sectors and include index-based positions

- Reduce position sizes after consecutive losing months; scale up only after consistent profitability

- The compound math of consistent small-risk sizing crushes the performance of oversized, undisciplined trading over any meaningful timeframe

What’s Next

You’ve now completed 20 articles building from foundational beginner concepts through intermediate income strategies, volatility tools, and professional risk management. The next series expands into deeper strategy territory — starting with the engine under the hood of every options price: What Is Implied Volatility — And Why Every Options Trader Must Understand It.

If you’re ready to put this full framework into practice, Tastytrade is the platform built for options-focused portfolio management — with buying power utilization, per-position Greeks, and portfolio-level delta all visible in one dashboard so you can track your exposure across every open trade simultaneously.

Disclosure: this is a referral link. If you sign up via this link, the site may earn a commission at no cost to you.

Disclaimer: This content is for educational and informational purposes only and does not constitute financial, investment, or trading advice. Options trading involves significant risk and is not suitable for all investors. You may lose the entire amount invested. Always conduct your own research and consult a licensed financial advisor before making investment decisions.